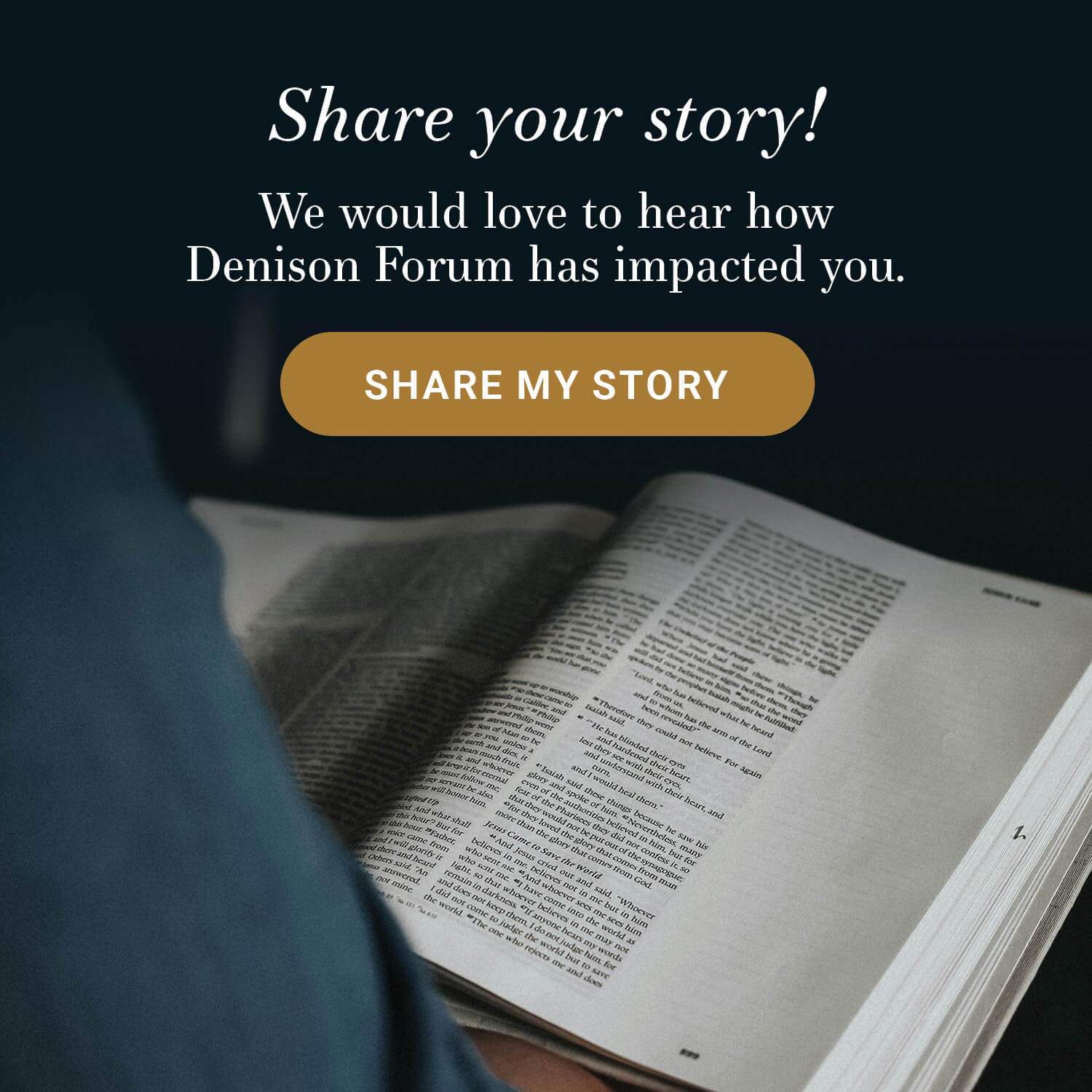

Security guards let individuals enter the Silicon Valley Bank's headquarters in Santa Clara, Calif., on Monday, March 13, 2023. The federal government intervened Sunday to secure funds for depositors to withdraw from Silicon Valley Bank after the bank's collapse. Dozens of individuals waited in line outside the bank to withdraw funds. (AP Photo/ Benjamin Fanjoy)

On Monday, spurred by the Silicon Valley Bank collapse, President Biden addressed the nation in the wake of the ongoing banking crises to reassure Americans that we “can have confidence that the banking system is safe. Your deposits will be there when you need them.”

Unfortunately, the stock market disagreed.

Trading on more than a dozen small to mid-sized banks was forced to halt after prices continued to free fall. However, the crisis seems fueled less by the fears of an impending bank run depleting available cash—emergency measures taken by the government over the weekend appear to have largely staved off that fear—than by concerns that what happened at Silicon Valley Bank last Thursday is a sign that the Fed’s attempts to control inflation through interest rate hikes “may be cracking the banking system.”

A closer look at what went wrong last week shows that such fears are not entirely unfounded.

SVB was not a normal bank

To understand the scope of the crisis that began last Thursday, it’s important to note that Silicon Valley Bank (SVB) was not a normal bank.

SVB got its start in the 1980s by investing in Silicon Valley startups and then providing a place for those startups to keep their investors’ money. As such, they’ve always leaned more heavily into the high-risk, high-reward technology sector than your average bank.

Whereas most financial institutions have a pretty diverse set of customers, SVB was primarily used by venture capitalists and small businesses. As much as 97 percent of its deposits went beyond the $250,000 limit insured by the FDIC and the average customer balance as of late last year was $4.2 million. Consequently, when customers attempted to withdraw roughly $42 billion last Thursday over fears that their money wasn’t safe in the bank, SVB ended the day in the red by more than $950 million.

Word quickly spread after screenshots of error messages from those who tried to access their funds went viral and the government stepped in last Friday to shut them down.

But while the Silicon Valley Bank collapse happened quickly, the signs had been there for some time.

What caused the Silicon Valley Bank collapse?

SVB’s largest problems stemmed less from the influx of people trying to get their cash than the ways that the bank had used that cash in recent years.

No bank carries enough currency to match the total amount deposited by its customers. Rather, they keep a percentage and reinvest the rest in loans, bonds, government securities, and other assets. That reinvestment is why they are able to pay interest on savings accounts and take on other forms of risk to help their clients.

The people running Silicon Valley Bank, however, leaned far more heavily into those risks than most.

As Vivek Ramaswamy notes, SVB invested roughly 57 percent of its total assets—its peer average is 24 percent—and of its $120 billion investment portfolio, only $26 billion was held in assets that were easy to move. The rest was tied up in bonds and securities that can be difficult to sell without taking a loss, especially in the current economic climate.

You see, well before SVB invested much of its pandemic-related growth in US treasury bonds and mortgage-backed securities, the Fed warned about inflation and the likelihood that they would raise interest rates in a way that could heavily jeopardize the value of those assets. SVB ignored those warnings and invested anyway.

As such, when they were forced to sell $21 billion in bonds over recent weeks at a nearly $2 billion loss, it set off red flags that culminated in the chaos of last Thursday.

However, given that SVB President Greg Becker sold roughly $3.6 million in company stock two weeks ago while urging investors to “stay calm,” it seems clear that present events were hardly a surprise.

Will the SVB collapse affect your finances?

So what happens now?

Unlike when the “too-big-to-fail” banks went under in 2007 and 2008, those in charge of SVB have already lost their jobs and the bank’s remaining assets are being sold off to help cover the cost of ensuring that the bank’s clients will have access to their money. Sunday night, HSBC bought the UK subsidiary of SVB for one pound—roughly $1.20—and a similar model could be pursued for the rest of SVB as well.

However, the larger threat to the banking system still looms.

As George Godber, a fund manager at Polar Capital, remarked, “The imminent crisis may have been averted but it’s alerted people to the fact that there’s a group of companies out there with business models who will struggle in a high-interest rate environment.” In short, people are worried that what happened to SVB could happen to their bank as well, even if the same risk factors don’t exist. And that fear—even though unfounded in most cases—has proven strong enough to potentially damage an entire industry.

Choosing faith over fear

One of the most difficult of Christ’s commands comes in the Sermon on the Mount when he instructs his disciples to “not be anxious about your life” (Matthew 6:25). In the Greek, that sense of anxiety carries the idea of being “divided into parts” or “drawn in opposite directions.”

The idea here is not that we never experience the emotion of fear—God never commands us how to feel. Rather, the sin against which we are warned is feeding our anxiety by dwelling on it instead of giving it back to God and trusting that he not only knows our needs but has a plan to meet them as well.

Fears over the present economic climate and whether your bank will be the next to go under are understandable. And they are hardly the only thing we have to be anxious about these days.

But it’s the times when fear seems like the most natural response that choosing faith can make the greatest impact on our lives and on our culture.

Which will you choose today?